Are Nurses Richer Than Doctors? It’s a question that sparks curiosity, and at thebootdoctor.net, we’re here to unravel the financial realities behind these two essential healthcare professions. While doctors often have higher earning potential, strategic financial planning, early investment, and lower educational debt can pave the way for nurses to accumulate significant wealth and even surpass some physician specialties financially. The path to financial well-being involves understanding compound interest, leveraging tax-advantaged retirement accounts, and making informed investment decisions.

1. Why Financial Planning Matters for Nurses

Nurses face unique challenges and opportunities in their careers, making financial planning a critical aspect of their professional lives.

1.1. Understanding the Importance of Time and Resource Management

Nursing is a demanding profession, and nurses quickly learn that time is a precious resource. This understanding extends to their personal finances, where early planning and consistent savings can lead to significant long-term gains. According to the American Nurses Association (ANA), nurses who prioritize financial planning experience reduced stress and improved overall well-being.

1.2. Recognizing the Physical, Mental, and Emotional Demands of Nursing

The physical, mental, and emotional demands of nursing can impact career longevity. Planning for retirement early allows nurses to have options and financial security, regardless of how long they choose to remain in direct patient care. The burnout rate among nurses is high, with many considering leaving the profession within the first five years. A solid financial plan can provide a safety net and the freedom to pursue other interests.

1.3. Planning for Retirement as a Nurse

Retirement planning may seem daunting, but it’s a crucial step for nurses to ensure a comfortable and secure future. By understanding different retirement savings options and implementing effective strategies, nurses can retire wealthier than many other professions. A recent study by Fidelity Investments showed that healthcare professionals who start saving early and consistently contribute to their retirement accounts accumulate significantly more wealth over time.

2. Basic Financial Principles for Nurses

Understanding basic financial principles is essential for nurses to make informed decisions about their money and investments.

2.1. Demystifying Finance and Investing

Finance and investing don’t have to be complicated. With a basic understanding of key concepts, nurses can take control of their financial future and make informed decisions about their money. According to a survey by the National Endowment for Financial Education (NEFE), individuals who understand basic financial concepts are more likely to save for retirement and manage their debt effectively.

2.2. The Power of Early Retirement Account Setup

Setting up retirement accounts early in your career can lead to substantial financial gains down the line. The earlier you start, the more time your investments have to grow through the power of compound interest. A report by the Employee Benefit Research Institute (EBRI) found that workers who start saving for retirement in their 20s are more likely to reach their retirement goals than those who start later in life.

2.3. Retiring Wealthier Than Doctors: A Realistic Goal

Believe it or not, it’s possible for nurses to retire wealthier than some doctors. By understanding and implementing smart financial strategies early, nurses can achieve financial independence and enjoy a comfortable retirement. This involves maximizing contributions to retirement accounts, investing wisely, and minimizing debt.

3. Why Nurses Can Excel Financially

Nurses possess several advantages that, when leveraged effectively, can lead to significant financial success.

3.1. High Demand for Nurses Nationwide

The nationwide demand for nurses creates ample opportunities to increase income and accelerate savings. With a growing shortage of nurses, many healthcare facilities offer competitive salaries, benefits, and incentives to attract and retain nursing talent. The Bureau of Labor Statistics projects that employment of registered nurses will grow 6 percent from 2022 to 2032, creating numerous job opportunities.

Nurse Counting Money

Nurse Counting Money

3.2. Lessons Learned from Fellow Nurses: Common Financial Challenges

Many nurses face similar financial challenges, such as delaying retirement planning due to perceived distance and complexity. Understanding these challenges and addressing them proactively is crucial for achieving financial success. According to a survey by the Transamerica Center for Retirement Studies, many workers, including nurses, underestimate the amount they need to save for retirement.

3.3. Overcoming the “Retirement Seems So Far Away” Mentality

It’s common to feel that retirement is too far off to worry about, but the reality is that starting early is crucial for maximizing long-term growth. The power of compound interest means that even small contributions made early in your career can grow into substantial sums over time.

3.4. The Impact of Starting Early: A Real-Life Example

Consider two nurses, both age 28, who contribute the same amount of money to their retirement accounts. One has been investing since age 23, while the other started this year (at 28). That five-year head start can lead to one nurse having significantly more money at retirement.

3.5. Simplifying the Retirement Account Setup Process

Setting up retirement accounts doesn’t have to be a daunting task. With readily available resources and guidance, nurses can easily set up their accounts and automate their savings. Many financial institutions offer online tools and resources to help individuals set up and manage their retirement accounts.

4. Where Not to Invest Your Money

Knowing where not to invest your money is just as important as knowing where to invest it.

4.1. Avoiding Bank Accounts and Under-the-Mattress Savings

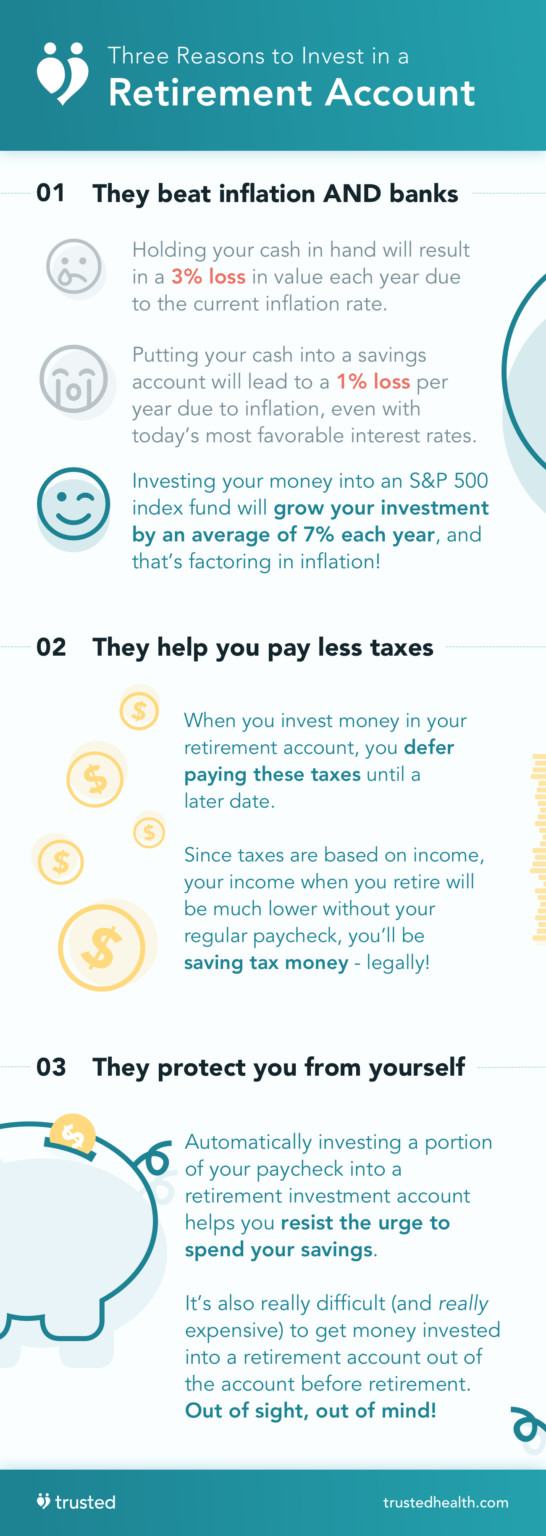

While it may seem safe to keep your money in a bank account or under your mattress, these options can actually lead to a loss of value over time due to inflation.

4.2. The Impact of Inflation on Savings

Inflation erodes the purchasing power of money over time. If your money is not earning a return that outpaces inflation, you are effectively losing money. The Federal Reserve Bank closely monitors inflation and aims to keep it within a target range.

4.3. Understanding Interest Rates and Their Limitations

While banks offer interest on savings accounts, the interest rates are often lower than the rate of inflation, resulting in a net loss of value. High-yield savings accounts offer slightly better interest rates, but they may still not keep pace with inflation.

4.4. Overcoming Lack of Willpower and Spending Habits

A lack of willpower can lead to impulsive spending and poor financial decisions. It’s important to develop healthy spending habits and avoid unnecessary purchases that can derail your financial goals. Creating a budget and tracking your expenses can help you stay on track.

4.5. Avoiding “Loser” Investments: Cars, Jewelry, and More

Certain purchases, such as new cars, jewelry, and clothing, are considered “loser” investments because they depreciate in value over time. While these items may provide enjoyment, they should be purchased with discretionary income and not at the expense of your financial goals.

5. Retirement Account Investing: Making Money While You Sleep

Retirement accounts offer a powerful way to grow your wealth and secure your financial future.

5.1. Beating Inflation with Retirement Accounts

Retirement accounts, when invested in assets like stocks and bonds, have the potential to outpace inflation and generate significant returns over time. The S&P 500 index, a benchmark for the U.S. stock market, has historically provided an average annual return of around 10%, well above the rate of inflation.

Retirement Account Investments

Retirement Account Investments

5.2. The Magic of Compound Interest

Compound interest is the process of earning interest on your initial investment as well as on the accumulated interest. This can lead to exponential growth over time, especially when you start early and consistently contribute to your retirement accounts.

5.3. Comparing Investment Growth: A Concrete Example

A $10,000 investment at age 30 that earns 2% annually will grow to a certain amount by the time you’re 65, while the same investment in an account that earns 7% annually will grow to a significantly larger amount in the same amount of time.

5.4. Paying Less Taxes with Retirement Accounts

Retirement accounts offer tax advantages that can help you save even more money. With traditional retirement accounts, you can defer paying taxes on your contributions until retirement, while with Roth accounts, your withdrawals in retirement are tax-free.

5.5. Solving Psychological Problems with Retirement Accounts

Retirement accounts can also help you overcome psychological barriers to saving, such as the temptation to spend your money. By automatically investing a portion of your paycheck into a retirement account, you can effectively remove the temptation to spend that money and ensure that you are saving for your future.

6. Investing in Your Freedom: Time Freedom

The ultimate goal of financial planning is to achieve financial independence and time freedom.

6.1. Accumulating Wealth and Generating More Wealth

By investing in assets that outpace inflation, you set yourself on a journey of accumulating wealth that generates more wealth. Over time, your investments can grow to the point where they generate enough income to cover your expenses, allowing you to achieve financial independence.

6.2. The Concept of Time Freedom

Time freedom is the state of having enough wealth that the annual return on your investments exceeds your expenses. When you reach this point, you are free to pursue your passions, spend time with your family, and live life on your own terms.

6.3. Why Nurses Deserve More Time

Nurses dedicate their lives to caring for others, and they deserve to have more time to spend with their families, pursue their passions, and enjoy life to the fullest. Financial planning can help nurses achieve this goal by providing them with the financial security and time freedom they deserve.

7. Nurses vs. Doctors: A Financial Comparison

While doctors often earn higher salaries, nurses have several financial advantages that can help them accumulate wealth.

7.1. The Financial Advantages of Nurses

Nurses typically start their careers with less student loan debt than doctors, allowing them to begin saving and investing sooner. They also have a shorter training period, which means they can start earning a full salary earlier in their careers.

7.2. The Impact of Medical School Debt on Doctors’ Finances

Doctors often accumulate significant student loan debt to pay for medical school, which can impact their ability to save and invest early in their careers. This debt can take years to pay off, delaying their progress towards financial independence.

7.3. A Spreadsheet Analysis: RNs vs. MDs

A spreadsheet analysis comparing the financial trajectories of nurses and doctors reveals that nurses can accumulate a similar amount of wealth as some physician specialties, especially if they start saving early and minimize their debt.

7.4. Sample Results for Doctors: Pediatricians, Internal Medicine, and Family Medicine

The analysis shows that doctors in lower-paying specialties, such as pediatricians, internal medicine physicians, and family medicine physicians, may have a similar level of wealth at retirement as nurses who start saving early and minimize their debt.

7.5. Sample Results for Nurses: ADN, BSN, and Early Graduates

Nurses with associate’s degrees in nursing (ADN) or bachelor’s degrees in nursing (BSN) can accumulate significant wealth over time, especially if they start saving early and minimize their debt. Nurses who graduate from nursing school at a younger age have an even greater advantage due to the power of compound interest.

Spreadsheet Example

Spreadsheet Example

7.6. The Impact of Graduate School: NPs and CRNAs

Nurses who pursue advanced degrees, such as nurse practitioners (NPs) or certified registered nurse anesthetists (CRNAs), can significantly increase their earning potential. However, it’s important to factor in the cost of tuition and the opportunity cost of lost income when considering whether to pursue graduate education.

8. Limitations of the Financial Comparison

It’s important to acknowledge the limitations of the financial comparison between nurses and doctors.

8.1. Higher-Earning Physician Specialties

The analysis focuses on lower-paying physician specialties. Doctors in higher-paying specialties, such as surgeons and anesthesiologists, typically accumulate significantly more wealth than nurses.

8.2. The Stress and Pressure of High-Paying Medical Specialties

While higher-paying medical specialties offer the potential for greater wealth accumulation, they also come with increased stress and pressure. The demands of these specialties can impact work-life balance and overall well-being.

8.3. Student Loan Debt Repayment Realities

The analysis simplifies the student loan debt repayment process. In reality, student loan debt repayment plans can be complex and may involve loan amortization schedules and income-driven repayment options.

8.4. Income Growth Over Time

The analysis does not account for income growth over time. In reality, both nurses and doctors typically experience income growth as they gain experience and advance in their careers.

9. Key Takeaways and Next Steps for Nurses

The key takeaways from this analysis are that debt matters, early investing is crucial, and choosing the right investment vehicles can make a significant difference in your financial outcome.

9.1. Debt Matters: Minimize Student Loan Debt

Graduating with minimal student loan debt is essential for maximizing your long-term financial potential. Explore scholarship opportunities, grants, and work-study programs to minimize your debt burden.

9.2. Early Investing is Crucial: Pay Off Debt and Start Saving STAT

Once you start working, prioritize paying off your debt as quickly as possible. Once your debt is paid off, start contributing to your retirement accounts immediately. Even small delays in investing can have a significant impact on your long-term wealth.

9.3. Invest in the Right Vehicles: Maximize Returns

Choose the right investment vehicles to maximize your returns. Consider investing in a diversified portfolio of stocks, bonds, and other assets. Consult with a financial advisor to determine the best investment strategy for your individual circumstances.

10. Take Control of Your Financial Future Today

Ready to take control of your financial future? Visit thebootdoctor.net for more valuable resources, articles, and guidance on financial planning for nurses. Contact us today to schedule a consultation with one of our financial experts.

FAQ: Are Nurses Richer Than Doctors?

10.1. Is it really possible for nurses to retire richer than doctors?

Yes, it is possible for nurses to retire wealthier than some doctors, particularly those in lower-paying specialties, by starting to save early, minimizing debt, and investing wisely.

10.2. What are the key financial advantages that nurses have over doctors?

Nurses typically have less student loan debt and a shorter training period, allowing them to start saving and investing earlier in their careers.

10.3. How does student loan debt impact doctors’ ability to save for retirement?

High student loan debt can delay doctors’ progress towards financial independence, as they need to allocate a significant portion of their income towards debt repayment.

10.4. What is the role of compound interest in building wealth?

Compound interest is the process of earning interest on your initial investment as well as on the accumulated interest, leading to exponential growth over time.

10.5. What are the best investment vehicles for nurses to consider?

Nurses should consider investing in a diversified portfolio of stocks, bonds, and other assets through retirement accounts such as 401(k)s and IRAs.

10.6. How can nurses minimize their student loan debt?

Nurses can minimize their student loan debt by exploring scholarship opportunities, grants, and work-study programs.

10.7. What are the tax advantages of retirement accounts?

Retirement accounts offer tax advantages such as tax-deferred growth or tax-free withdrawals, which can help individuals save even more money for retirement.

10.8. How can nurses overcome psychological barriers to saving?

Nurses can overcome psychological barriers to saving by automating their savings and setting clear financial goals.

10.9. What is time freedom and how can nurses achieve it?

Time freedom is the state of having enough wealth that the annual return on your investments exceeds your expenses, allowing you to pursue your passions and live life on your own terms. Nurses can achieve time freedom through financial planning and smart investing.

10.10. Where can nurses find more resources and guidance on financial planning?

Nurses can find more resources and guidance on financial planning at thebootdoctor.net, which offers articles, tools, and expert consultations.

At thebootdoctor.net, we’re dedicated to providing you with the information and resources you need to achieve your financial goals. Whether you’re just starting your nursing career or you’re well on your way to retirement, we’re here to help you every step of the way. Contact us today at Address: 6565 Fannin St, Houston, TX 77030, United States, Phone: +1 (713) 791-1414, Website: thebootdoctor.net to learn more about how we can help you secure your financial future.