Are Doctors Paid During Residency? Yes, doctors are paid during their residency in the United States. This compensation, while providing financial relief after years of medical school, often necessitates careful financial planning due to long hours and significant debt. The experts at thebootdoctor.net provide insights into the realities of resident salaries and managing finances during this demanding period.

This guide provides a detailed look into resident compensation, work expectations, and financial challenges. Understand resident income, physician salaries, and financial well-being with our expert advice.

1. Understanding Resident Compensation in the U.S.

Yes, resident doctors in the U.S. receive a salary. However, it’s essential to understand the details of this compensation, considering the demands and financial challenges of residency. Let’s examine the nuances of resident pay.

1.1. Average Resident Salary

The average salary for a resident in the US is approximately $67,400 as of 2023, according to a Medscape report. While this figure provides a general benchmark, actual salaries can vary based on the specialty, location, and year of training. Understanding the factors that influence resident pay can help aspiring doctors plan their finances more effectively.

1.2. Factors Influencing Salary

Several factors determine a resident doctor’s salary:

- Specialty: Some specialties, such as those requiring more on-call hours or demanding higher levels of expertise, may offer slightly higher compensation.

- Location: Geographic location plays a significant role due to differences in the cost of living and hospital funding. For instance, residents in urban areas may receive higher salaries to offset higher living expenses.

- Year of Training: As residents advance through their training, their salaries typically increase, reflecting their growing experience and responsibilities.

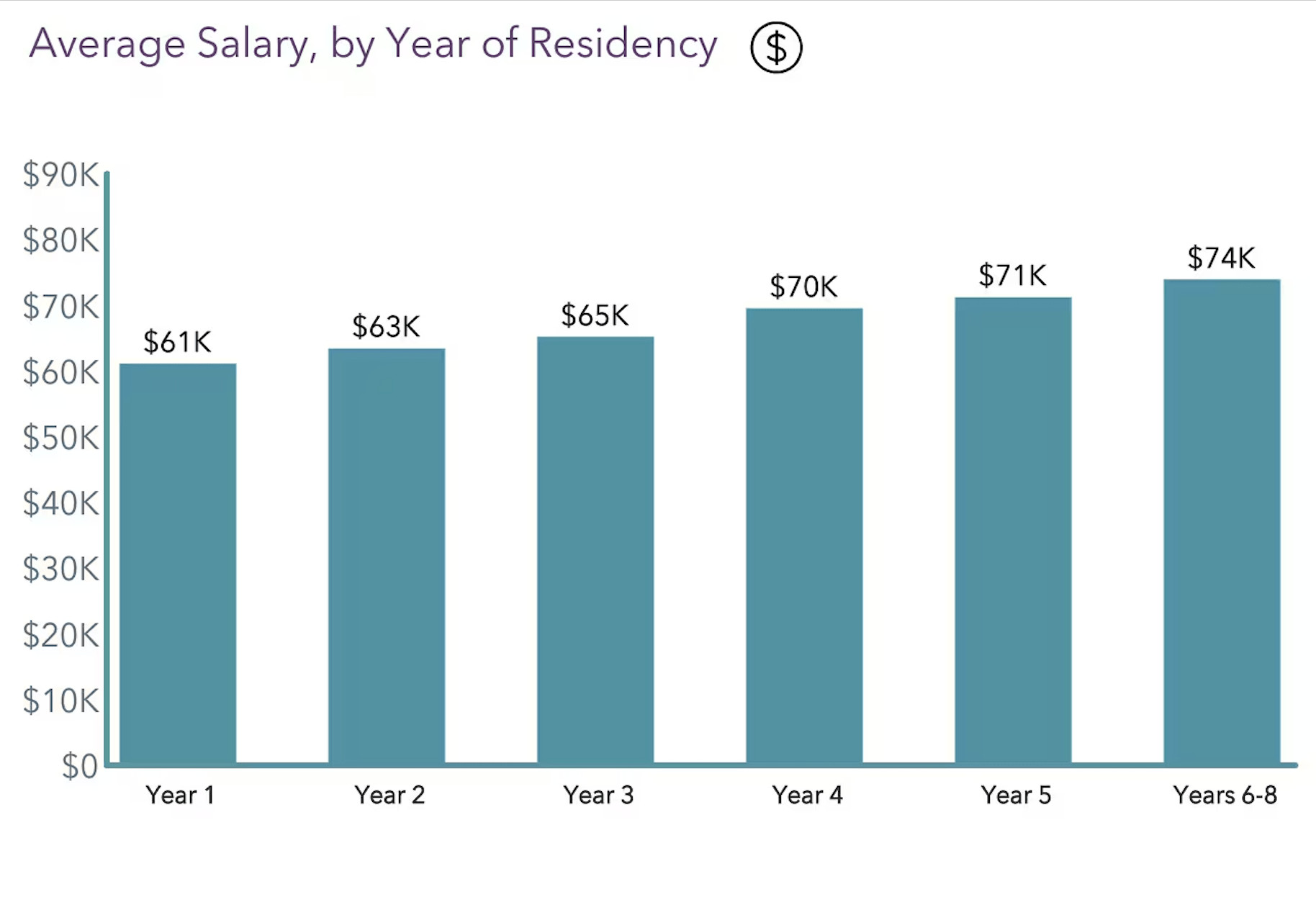

1.3. Salary Progression During Residency

Resident salaries increase incrementally throughout the training period. While the initial salary might be modest, it gradually rises, providing some financial relief as residents gain experience. However, these increases are often small compared to the earnings of fully licensed physicians.

Average salary by year of residency chart

Average salary by year of residency chart

1.4. Comparison with Other Healthcare Professionals

When considering resident compensation, it’s helpful to compare it with other healthcare professionals. Mid-level providers, such as Nurse Practitioners (NPs) and Physician Assistants (PAs), may earn comparable or even higher salaries than residents while often having less debt and shorter training periods. This comparison highlights the financial sacrifices residents make to pursue their medical careers.

1.5. How Residency Salaries Are Determined

Residency salaries are determined by a combination of factors, including hospital budgets, Medicare funding, and collective bargaining agreements. Teaching hospitals, which often host residency programs, receive Medicare funding to support graduate medical education (GME). These funds are allocated to resident salaries and program costs, influencing the overall compensation structure.

1.6. Impact of Cost of Living on Resident Salaries

The cost of living significantly impacts the financial well-being of resident doctors. In high-cost urban areas, a resident salary may barely cover basic living expenses, leading to financial strain. Conversely, residents in more affordable regions may find their salaries more manageable. Resources like thebootdoctor.net can help residents navigate these financial challenges by providing budgeting tips and financial planning advice.

2. Decoding the Resident’s Hourly Wage

It’s essential to consider the hourly rate of residents, given their rigorous schedules. The Accreditation Council for Graduate Medical Education (ACGME) has set limits on resident work hours to protect against overwork, yet these rules are not always followed, and schedules remain demanding.

2.1. Calculating the Hourly Rate

Calculating the hourly rate for a resident involves dividing their annual salary by the number of hours worked per year. Considering the average resident salary of $67,400 and assuming a 60-hour work week, the hourly rate is approximately $21.50. However, if a resident works more than 80 hours per week, the hourly rate drops significantly, sometimes falling below minimum wage in certain states.

2.2. The Impact of Long Hours

Long work hours are a defining characteristic of residency. While the ACGME mandates an 80-hour weekly limit, many residents exceed this, leading to burnout and reduced hourly pay. The implications of these extended hours can affect residents’ mental and physical health, making it crucial to understand and address this issue.

2.3. Factors Affecting Hourly Rate

Several factors affect the hourly rate of resident doctors:

- Specialty: Certain specialties require more time on call, affecting the actual hours worked.

- Institution: Some hospitals and training programs may have better adherence to work-hour regulations.

- Year of Training: As residents progress, their responsibilities may shift, impacting their hours.

2.4. Minimum Wage Concerns

In some cases, when residents work extremely long hours, their effective hourly rate can fall below the minimum wage. This raises ethical concerns about the value placed on their labor and the need for fair compensation practices. It also highlights the importance of advocating for better working conditions and fair wages for resident doctors.

2.5. Strategies for Managing Long Hours

Given the demanding nature of residency, it is essential for residents to adopt strategies for managing long hours. Some helpful approaches include:

- Time Management Techniques: Prioritizing tasks, setting realistic goals, and using time-tracking tools can help residents make the most of their limited time.

- Seeking Support: Building a strong support network of colleagues, mentors, and family members can provide emotional and practical assistance during challenging times.

- Advocating for Change: Residents can advocate for better working conditions and fair compensation by participating in organized labor efforts and voicing their concerns to program administrators.

2.6. The Role of Unions in Protecting Residents

Unions play a critical role in protecting residents’ rights and advocating for fair compensation and working conditions. By collectively bargaining with hospitals and training programs, unions can secure better wages, benefits, and protections against overwork. Residents who are members of unions often report higher levels of job satisfaction and improved financial well-being.

3. The Financial Burden of Medical Training

The financial burden of medical training can be staggering, with many doctors burdened by substantial debt. It’s important to address this issue and look at ways to alleviate the financial strain.

3.1. Average Medical School Debt

The average medical school debt is approximately $250,000. High tuition fees, living expenses, and interest rates contribute to this substantial burden. This debt can significantly impact a resident’s financial well-being and long-term financial goals.

3.2. Interest Rates and Accrual

Interest rates on medical school loans can range from 6% to over 8%, leading to significant accrual over the repayment period. Even while residents make payments, a substantial portion often goes toward interest, barely reducing the principal debt. Understanding the impact of interest rates is crucial for effective debt management.

3.3. Impact on Lifestyle and Savings

The heavy debt burden can significantly impact a resident’s lifestyle and savings. Many residents delay major life decisions, such as buying a home or starting a family, due to financial constraints. Saving for retirement and other long-term goals becomes challenging.

3.4. Debt Management Strategies

Effective debt management strategies can help residents alleviate the financial strain. These strategies include:

- Income-Driven Repayment Plans (IDR): IDR plans, such as Income-Based Repayment (IBR) and Pay As You Earn (PAYE), cap monthly payments based on income and family size.

- Loan Forgiveness Programs: Programs like Public Service Loan Forgiveness (PSLF) offer loan forgiveness after ten years of qualifying employment in a non-profit or government organization.

- Refinancing: Refinancing medical school loans at a lower interest rate can reduce monthly payments and overall interest paid.

3.5. Budgeting and Financial Planning

Creating a detailed budget and financial plan is essential for residents. Tracking income and expenses, setting financial goals, and seeking professional advice can help residents make informed decisions. Thebootdoctor.net offers resources and guidance on budgeting and financial planning tailored to resident doctors.

3.6. The Importance of Financial Literacy

Financial literacy is crucial for resident doctors to make informed decisions about their finances. Understanding basic financial concepts, such as budgeting, investing, and debt management, can help residents build a solid financial foundation. Financial literacy programs and resources can empower residents to take control of their financial futures.

4. Resident Finances: A Hypothetical Monthly Breakdown

Understanding the monthly finances of a resident doctor can provide a clear picture of their financial situation. Let’s break down a hypothetical budget based on average figures.

4.1. Income and Taxes

Based on an average salary of $67,400 per year, a resident’s gross monthly income is approximately $5,600. After federal and state taxes (assuming zero state tax), the net monthly income is reduced to around $4,600.

4.2. Debt Payments

The average medical school debt requires a monthly payment of at least $500 under an income-driven repayment plan, reducing the available income to $4,100. However, this minimum payment often barely covers the interest, leading to accrued debt.

4.3. Housing and Utilities

The average rent in the US is around $1,400 per month. After including utilities, the total housing cost may amount to $1,700, leaving approximately $2,400.

4.4. Groceries and Transportation

A low grocery budget for one person is about $300, and transportation costs average $500 per month, further reducing the available income to $1,600.

4.5. Other Expenses

Additional expenses, such as dining out, phone bills, fitness expenses, medical expenses, and insurance, can quickly consume the remaining funds. Unexpected costs, such as emergencies, can create additional financial strain.

4.6. Savings and Investments

Given these expenses, saving and investing can be challenging for residents. Contributing to retirement accounts and building an emergency fund often take a backseat to managing debt and covering basic living expenses.

4.7. How to Optimize Your Monthly Finances

Optimizing monthly finances is essential for resident doctors. Creating a detailed budget, tracking expenses, and identifying areas for savings can help residents make the most of their limited income. Seeking financial advice and exploring options for debt management can also improve financial well-being.

5. Resident Satisfaction with Compensation

It’s important to look at how residents feel about their pay. Compensation satisfaction is a key factor affecting motivation and overall well-being.

5.1. Survey Results and Statistics

According to a 2023 Medscape report, only 20% of residents feel fairly compensated for their work. Dissatisfaction often stems from long hours and a sense that their pay doesn’t reflect the value of their contributions.

5.2. Reasons for Dissatisfaction

Residents who are dissatisfied with their compensation often cite the following reasons:

- Long Hours: The perception that their pay doesn’t match the hours they work.

- Comparison with Other Medical Staff: The feeling that they are underpaid compared to other healthcare workers with similar levels of responsibility.

- Financial Stress: The strain of managing debt and covering living expenses on a limited income.

5.3. Factors Influencing Satisfaction

Factors that influence satisfaction with compensation include:

- Specialty: Some specialties may offer better compensation packages, leading to higher satisfaction.

- Location: Cost of living and local market conditions can affect residents’ perception of their pay.

- Program Support: Supportive residency programs that offer resources and benefits can improve overall satisfaction.

5.4. Impact on Performance and Well-being

Dissatisfaction with compensation can negatively impact resident performance and well-being. Financial stress can lead to burnout, reduced motivation, and compromised patient care. Addressing compensation concerns is crucial for maintaining a healthy and productive workforce.

5.5. Strategies for Improving Satisfaction

Residency programs can implement strategies to improve resident satisfaction with compensation, such as:

- Transparent Communication: Clearly communicating how salaries are determined and addressing concerns openly.

- Fair Compensation Practices: Ensuring that pay reflects the value of residents’ contributions and is competitive with other programs.

- Financial Wellness Programs: Providing resources and support for financial planning and debt management.

5.6. Advocacy for Fair Pay

Advocating for fair pay is essential for improving resident satisfaction. Residents can participate in organized labor efforts, voice their concerns to program administrators, and support policies that promote fair compensation for resident doctors.

6. Making Informed Career Decisions

Making informed career decisions is critical for aspiring doctors. Understanding the financial implications of pursuing a medical career can help individuals make choices that align with their goals.

6.1. Long-Term Financial Outlook

While residency salaries may be modest, the long-term financial outlook for licensed physicians is generally favorable. However, it’s important to consider the time and investment required to reach that point.

6.2. Weighing Costs and Benefits

Aspiring doctors should carefully weigh the costs and benefits of a medical career. Factors to consider include:

- Tuition Fees: The cost of medical school can be substantial.

- Living Expenses: Housing, transportation, and other living expenses can add up during training.

- Opportunity Costs: The income that could be earned in other careers during the years spent in medical school and residency.

6.3. Considering Alternatives

Exploring alternative career paths in healthcare may be prudent for some individuals. Options such as becoming a Nurse Practitioner or Physician Assistant offer shorter training periods and potentially comparable salaries.

6.4. Financial Planning Early On

Starting financial planning early in medical school can help students make informed decisions about borrowing and debt management. Developing a budget, tracking expenses, and seeking financial advice can provide a solid foundation for future financial success.

6.5. Researching Specialties

Different specialties offer varying levels of compensation. Researching the earning potential and job market outlook for different specialties can help aspiring doctors choose a path that aligns with their financial goals.

6.6. Mentorship and Guidance

Seeking mentorship and guidance from experienced physicians and financial advisors can provide valuable insights and support. Mentors can share their experiences and offer advice on navigating the financial challenges of a medical career.

7. Tips for Managing Finances During Residency

Managing finances during residency requires careful planning and discipline. Here are some practical tips to help residents make the most of their limited income:

7.1. Creating a Budget

Creating a detailed budget is the first step toward effective financial management. Track income and expenses, identify areas for savings, and set realistic financial goals.

7.2. Tracking Expenses

Use budgeting apps or spreadsheets to track expenses and monitor spending patterns. This can help identify areas where costs can be reduced.

7.3. Reducing Debt

Explore options for reducing debt, such as refinancing loans at a lower interest rate or consolidating multiple loans into one.

7.4. Automating Savings

Set up automatic transfers to savings accounts to ensure regular contributions. Even small amounts can add up over time.

7.5. Living Frugally

Adopt a frugal lifestyle by cooking meals at home, using public transportation, and avoiding unnecessary expenses.

7.6. Seeking Financial Advice

Consult with a financial advisor to develop a comprehensive financial plan and receive personalized guidance on debt management, investing, and retirement planning.

8. Resources for Resident Doctors

Numerous resources are available to support resident doctors in managing their finances and navigating the challenges of residency.

8.1. Financial Aid Offices

Financial aid offices at medical schools can provide information on loan repayment options and financial resources.

8.2. Professional Organizations

Professional organizations, such as the American Medical Association (AMA), offer resources and support for resident doctors, including financial planning tools and advice.

8.3. Online Resources

Websites like thebootdoctor.net offer articles, guides, and tools to help residents manage their finances and make informed decisions.

8.4. Support Groups

Support groups and online communities provide a platform for residents to connect, share experiences, and offer advice on financial and professional challenges.

8.5. Mental Health Services

Residency can be stressful, and mental health services are essential for maintaining well-being. Many residency programs offer counseling and support services to help residents cope with stress and burnout.

8.6. Mentorship Programs

Mentorship programs connect residents with experienced physicians who can provide guidance and support on career and financial matters.

9. The Future of Resident Compensation

The future of resident compensation is an ongoing topic of discussion and advocacy. Efforts are being made to improve pay, benefits, and working conditions for resident doctors.

9.1. Advocacy Efforts

Advocacy efforts by professional organizations, unions, and resident advocacy groups aim to improve resident compensation and working conditions.

9.2. Policy Changes

Policy changes at the federal and state levels could lead to increased funding for graduate medical education (GME) and improved pay for resident doctors.

9.3. Program Initiatives

Residency programs are implementing initiatives to improve resident well-being, such as reducing work hours, providing financial wellness programs, and offering mental health services.

9.4. Collective Bargaining

Collective bargaining by resident unions can lead to better wages, benefits, and protections against overwork.

9.5. Transparency and Accountability

Increased transparency and accountability in residency programs can help ensure fair compensation practices and adherence to work-hour regulations.

9.6. The Role of Technology

Technology can play a role in improving resident compensation and well-being. Telemedicine, electronic health records, and other technologies can streamline workflows, reduce administrative burdens, and improve work-life balance.

10. Frequently Asked Questions (FAQs)

Addressing common questions about resident compensation can provide clarity and valuable information for aspiring and current resident doctors.

10.1. Do all residency programs pay the same?

No, residency program salaries can vary based on location, specialty, and hospital funding.

10.2. Are residents eligible for benefits?

Yes, residents are typically eligible for benefits such as health insurance, retirement plans, and paid time off.

10.3. Can residents work extra jobs to earn more money?

Some residency programs allow moonlighting, but it is subject to program approval and work-hour restrictions.

10.4. How can I negotiate my resident salary?

While resident salaries are generally fixed, you can negotiate benefits and other perks, such as housing stipends or professional development funds.

10.5. What is the Public Service Loan Forgiveness (PSLF) program?

PSLF forgives the remaining balance on Direct Loans after 120 qualifying monthly payments made under a qualifying repayment plan while working full-time for a qualifying employer.

10.6. How do income-driven repayment plans work?

Income-driven repayment plans cap monthly payments based on income and family size and offer loan forgiveness after a set number of years.

10.7. What is the best way to create a budget?

Start by tracking your income and expenses, setting financial goals, and identifying areas for savings. Use budgeting apps or spreadsheets to monitor your spending.

10.8. Should I refinance my medical school loans?

Refinancing can lower your interest rate and monthly payments, but consider the potential drawbacks, such as losing federal loan protections.

10.9. How can I improve my credit score?

Pay bills on time, keep credit card balances low, and avoid opening too many new accounts.

10.10. Where can I find reliable financial advice for residents?

Consult with a financial advisor, seek guidance from professional organizations, and explore online resources like thebootdoctor.net.

Understanding the financial aspects of residency is critical for aspiring and current doctors. While residency salaries may not be high, careful planning, budgeting, and debt management can help residents navigate the challenges and build a strong financial foundation. Explore more articles, guides, and resources at thebootdoctor.net to support your financial well-being. Find reliable information and expert advice at thebootdoctor.net. Contact us at 6565 Fannin St, Houston, TX 77030, United States or call +1 (713) 791-1414.